In a market economy, there is an interesting phenomenon called “Strategic Discontinuities”.

“Strategic discontinuities are major, often unanticipated, events that fundamentally change an industry or market, forcing companies to adapt their strategies to survive or seize new opportunities. These shifts can stem from technological, business model, regulatory, or social changes and often render past strategies obsolete, requiring a radical change in how a company operates.”

One of the early proponents of developing growth strategies around “ discontinuities” in the Indian IT services industry was Phaneesh Murthy, of Infosys and iGate fame. Mr.Murthy applied this concept effectively to pioneer what became known as the Global Delivery Model (GDM). This model created a strategic discontinuity in the software services industry, which was leveraged by Infosys resulting in its revenue growing from $2 million in 1987 to $700 million in under 10 years.

“When Murthy joined Infosys in the early 1990s, the company had spent its first decade growing from zero to just $1 million in revenue.The path to accelerating this growth came through recognizing an emerging discontinuity: the potential for a new operating model that would deliver technology services “faster, cheaper, better from India.”

Source : https://www.itsecurityguru.org

Strategic Discontinuity - In The Mobile VAS Industry

I started my sales career in the year 2003; having worked for a year as an installation & commissioning engineer for Telecom service providers & its service partners.

Incidentally, my pre-sales & sales journey started at Tecnomic, which was at that time a Value added Distributor for Intel-Dialogic, a business unit of Intel corporation.

Dialogic was a very popular name those days in the enterprise telephony space similar to what Nvidia is today for GenAI. Of course, not in terms of the revenue but in terms of its brand identity in the telephony domain.

“ In 1999, Intel acquired Dialogic for $780 million to expand its presence in computer telephony and communication technologies.”

The closest competition to Dialogic was NMS communications. Both these companies sold E1 cards with on-board DSPs, primarily for media processing and signalling; used by VAS application developers (IVRS, call recording, Dialler, SMSC, USSD Gateway, etc). These brands played a major role in the evolution of the VAS industry in India.

Somewhere around 2000, many startups around the world were working on a new category of applications that would be hosted within the Telco data centres. These applications delivered various content based services to mobile subscribers using the core infrastructure of Telecom companies. Such services came to be known as mobile VAS ( Value Added Services).

“The most exciting & innovative VAS market in terms of variety and scale handling was undoubtedly the Indian market driven by Cricket and Bollywood !”

The Bet That Changed Telecom VAS

When mobile operators in India were busy with their network roll outs, a VAS platform company called Onmobile was founded by Arvind Rao and Mouli Raman in the year 2000. Onmobile was incubated within the software services giant Infosys (The same company that pioneered the Global Delivery Model).

Typically, the VAS applications providers pitched their service delivery platforms to Telcos based on the CAPEX model. However, the Telcos were reluctant to divert their capital from deploying their core network services to unproven VAS services with a high risk-return profile. This was an opportune moment for a “strategic discontinuity” phenomenon to take root in the mobile VAS industry.

The anecdotal story goes this way :- Sometime in the year 2002, Onmobile shut down its US operations to focus on the Indian market. This was Arvind Rao, the maverick CEO of Onmobile making a big bet on India’s telecom market.

In one of his meetings with Orange telecom, Mumbai, he made a business call that would change his company’s fortunes forever. During that meeting, Orange offered a share of the actual revenue generated from its subscribers that used Onmobile’s services instead of paying upfront for the platform. Arvind Rao, the ex-Mackinsey & Co technology advisor, readily agreed to the offer and the rest as they say is history. The “Revenue share model” resulted in a “ Strategic Discontinuity” in the mobile VAS services industry and became the de-facto business model for VAS services not only in India but across the globe. Onmobile went on to become the number one VAS player in the world by 2010 both in terms of revenue and the number of subscribers served.

“With over 100 million subscribers for its services, including for the once wildly popular ringback tune, Onmobile grew rapidly from just over Rs 2 crore in income in 2002 to over Rs 500 crore by 2010.” Source: The internet.

The VAS industry tapered down post 2015, mostly due to the proliferation of OTT services riding on the 4G network & the evolution of advanced smart phone apps. In the meantime, most of the Indian VAS application companies had diversified into different domains like gaming, digital payments, CPaaS & CCaaS driven by the evolving technologies like 4G, Cloud computing and AI.

Snippet: The mobile 4G network created a major disruption in the market resulting in the “Blue Ocean strategy” adopted by app based aggregators like Uber & Ola and quick commerce services like Swiggy, Zomato & Zepto to create a new business segment heralding a new age in service delivery.

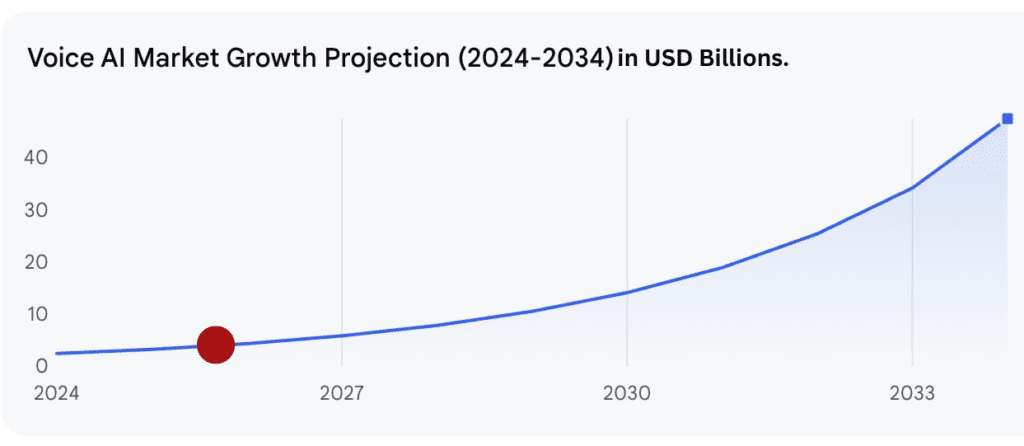

VoiceAI, on the cusp of the growth curve.

Source : https://market.us/report/voice-ai-infrastructure-market/

In the first decade of this century, the speech recognition technology pioneered by Nuance (later acquired by Microsoft) was seen as a high tech addition to the self care CX use cases, allowing users to speak to the IVR systems, instead of relying on the DTMF (Dual Tone Multi Frequency) keypads. However, the DSP based Speech recognition algorithm had failed to make an impact in the customer self-service space as a supplementary technology to IVRS even after two decades ( it was first launched by Nuance in 1996).

All this changed post 2016 when open source NLP( Natural Language Processing) platforms like Rasa got popular with developers. These ML based models, a predecessor to LLMs, were instrumental in re-establishing Voice as the most preferred channel for customer engagement providing an intuitive human-like experience. The good old IVRS had finally found its replacement.

With the rapid proliferation of GenAI based LLMs backed by big tech companies, the VoiceAI applications may become ubiquitous in the CX industry creating a competitive advantage to its early adopters.

Although LLM based VoiceBots are creating considerable buzz in the CX industry and work like magic as a standalone technology demonstrator, there are many challenges that application developers and solution architects have to overcome before they are able to deploy their applications at scale.

Common Challenges Faced by Voice AI Solution Providers

- Achieving Scalability and distributed architecture.

- High Infrastructure Costs – Finding ways to optimise resource usage on Cloud servers & third party speech modules.

- Compliance – Meeting regulatory requirements.

- Data Security – The system should be infrastructure agnostic to adhere to the infosec requirements of large organisations.

- Billing and revenue models – Flexibility to adopt evolving billing models.

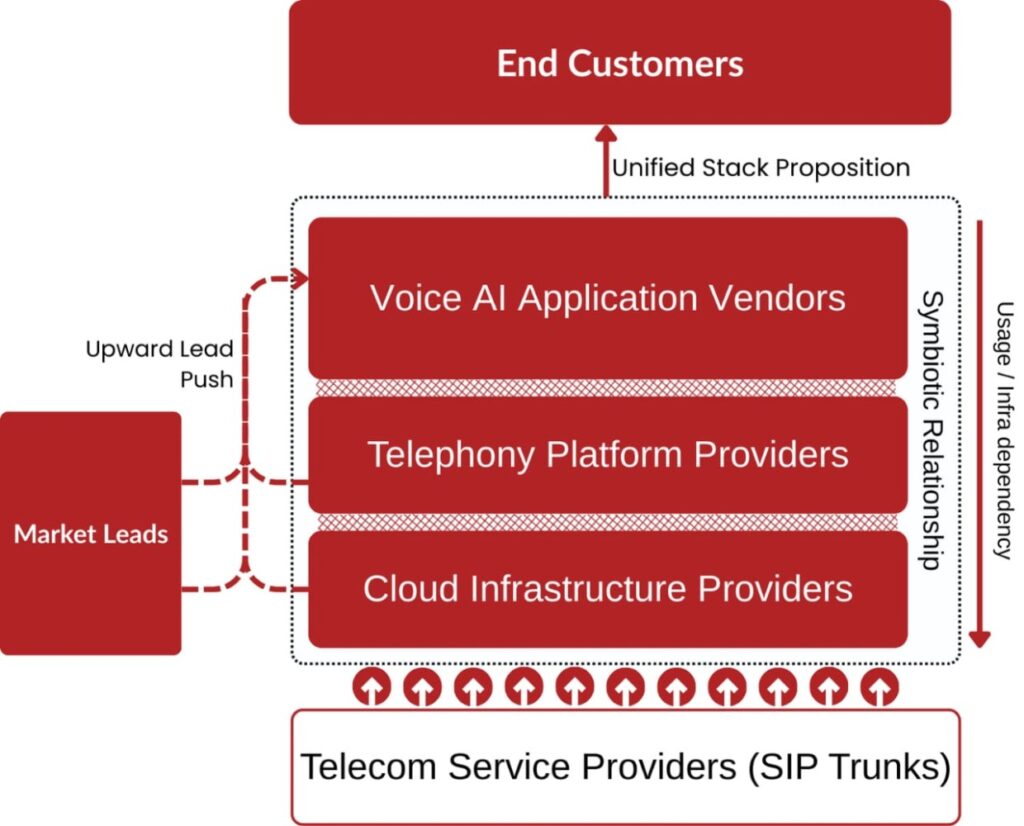

Incidentally, many of the challenges stated above cannot be wholly addressed by the application vendors since a full stack VoiceAI solution includes modules from multidisciplinary technology domains. It would be imprudent and unviable to address these challenges all by a single vendor. This is where the “ Best of breed” approach can create a competitive advantage. The trick is to work closely with third party technology & services partners with complementary expertise to create a seamless full stack solution that can address all of the above mentioned challenges and deliver a unified solution to the end customer. This can be achieved by cultivating what is known as a “ Collaborative Value chain” for the VoiceAI ecosystem.

Collaborative Value Chain

To understand “Collaborative Value Chain ” in our context, Let us consider the example of the VoiceBot use case. A VoiceBot solution typically consists of five distinct layers:

- The Application layer – Bot flow code integrated with KB, CRM & Campaign manager.

- The AI based Speech modules layer – TTS, STT & LLM.

- The Telephony layer – The telephony stack to connect to PSTN.

- The Infrastructure layer – Datacentres, to host all of the above.

- Telecom Core network – Telecom Service Providers.

There are a few players in the market offering a Full stack VoiceAI suite developed in-house. This approach is very resource intensive. The majority of such companies in India are finding it difficult to create & sustain multi disciplinary teams with expertise in GenAI, Telephony, distributed architecture, and business domain knowledge.

On the other hand, VoiceAI startups, CX Systems Integrators, AI products companies, and messaging CPaaS players are applying a “best-of-breed” strategy to build their VoiceAI stack. These companies are well positioned to address fast-evolving VoiceAI use cases more effectively due to their agility and by playing to their strengths. They seem to have adopted a customer centric approach with focus on solving business problems rather than a platform centric approach, which is capital intensive. This approach allows them to have shorter GTM timeframes, reduce development costs and scale faster. In order to put together an effective and scalable full stack voiceAI solution involving third party modules, it is essential to foster a “Collaborative Value Chain ( CVC)”.

These AI solution companies adopting the “ Best of Breed” approach primarily focus on the AI application and business intelligence layer ( customer domain specific) while depending on third party telephony stack providers ( who in turn manage the complexities pertaining to data centre & telecom core Infrastructure) to address the telephony and core network challenges. This division of responsibility based on domain expertise is key to develop a hyper scalable and resilient full stack VoiceAI platform.

The pre-requisites for creating a “ Collaborative Value Chain” requires that the stakeholders, which form an integral part of the Unified VoiceAI stack, have to put in place a joint working group that can work closely to continuously optimise the entire VoiceAI tech stack to make it competitive and to implement collective marketing strategies. The following objectives could be achieved through an effective CVC:

- Resource optimisation to reduce costs.

- Develop tech hacks to reduce AI token usage.

- Optimise the deployment architecture to reduce latency and bandwidth usage.

- Arrive at a mutually beneficial and flexible pricing model.

- Agree on the division of labour and responsibility matrix.

- Collaborate on Joint marketing efforts.

- Proactive lead generation by all stakeholders resulting in a force multiplier effect.

Conclusion

The CVC consortium should approach the market as a unified block instead of merely establishing a transactional relationship.

An effective VoiceAI CVC working group can potentially create a “Strategic Discontinuity” from the business model perspective to create a clear competitive advantage to all the stakeholders including the end customers.

I was fortunate to have experienced the ” Strategic Discontinuity” phenomenon play out in the mobile VAS industry as a young sales executive. Those days, I used to sell telephony hardware to all the major VAS players like Onmobile, One97 ( PayTM), IMI Mobile, Tanla, Comviva, 6D technologies, CanvasM, etc. Today, as a co-founder of Epicode, which is part of the thriving VoiceAI ecosystem, I find myself once again in the midst of a ” Strategic Discontinuity” taking shape in the VoiceAI market. I hope this turns out to be another roller coaster ride !